Zoetis is the alpha dog of the pet economy

Amid shrinking households and declining birth rates, one family member is increasingly taking centre stage: the pet. Half of Americans consider their pets to be as much a part of the family as human members, with pets now outnumbering children in households across the US. Within this thriving market sits Zoetis (pronounced “zoh-eh-tis”) - the world’s largest animal health company.

Originally part of Pfizer, Zoetis was spun off in 2013 and has since forged its own path as the leader in animal healthcare. We examine Zoetis’ role at the forefront of this expanding market.

A winning portfolio

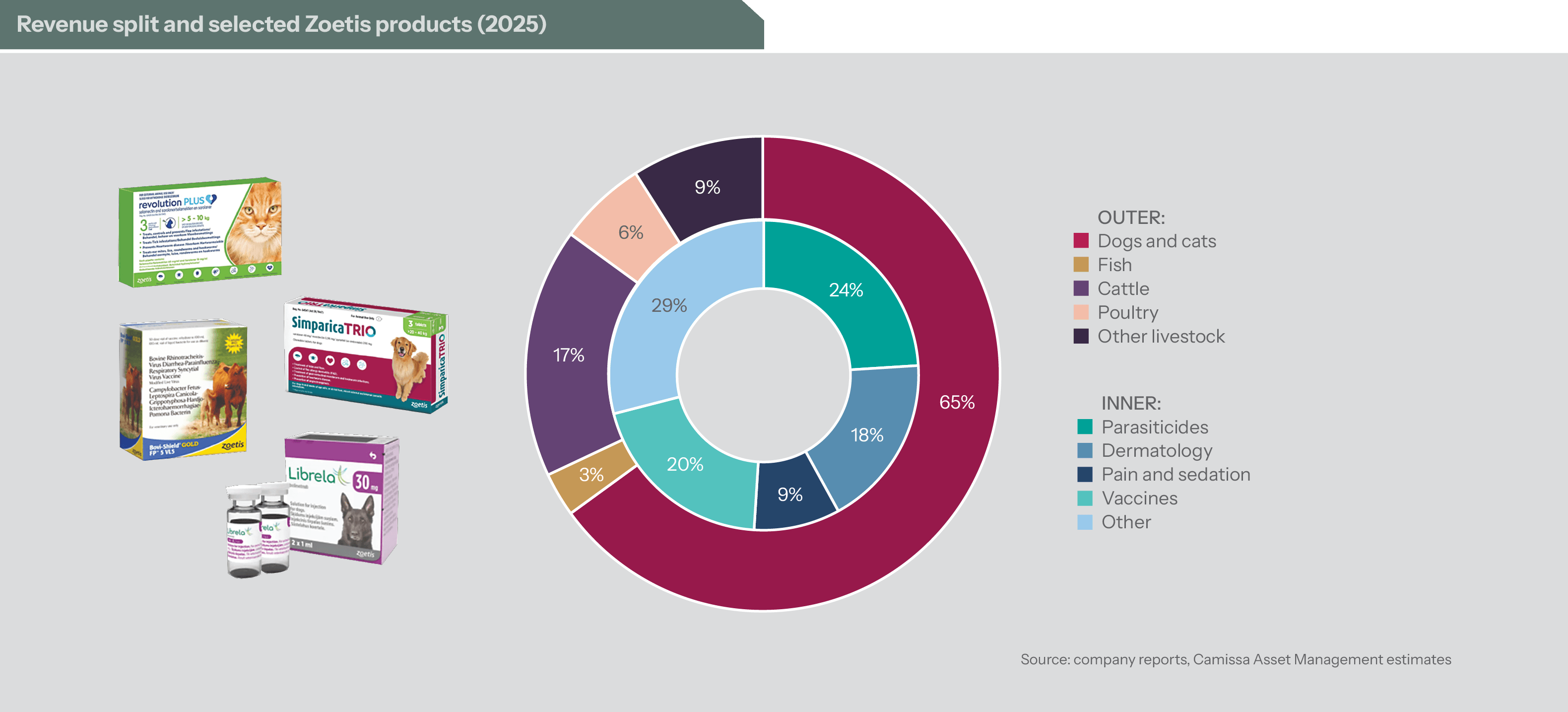

Zoetis offers a portfolio of high-quality, high-margin vaccines and medicines for both companion animals and livestock - illustrated below. The company markets over 300 products across more than 100 countries, addressing conditions such as parasites, pain management and dermatitis. Currently, the US constitutes 55% of revenue for the business.

A product that highlights Zoetis' competitive edge is Simparica Trio, a once-monthly chewable tablet for dogs that provides protection against fleas, ticks and heartworm. It was the first triple-action parasiticide on the market and, since its launch in 2020, has surpassed $1 billion in annual sales to become the top selling parasiticide in the US.

Its success reflects a simple but powerful insight: reaching pet owners early - ideally at a puppy’s first veterinarian visit - creates compelling long-term economics. A satisfied owner who starts their dog on Simparica Trio in puppyhood is, in all likelihood, a customer for the next 12 to 15 years. This industry strategy is known as "winning the puppy".

Approximately 95% of Zoetis’ product portfolio is prescription-only, making vets critical commercial gatekeepers. Vets are cautious by nature and therefore, once a product has proven safe and effective, they are reluctant to switch. Zoetis engages deeply with the veterinarian channel, investing in bursaries, education and expanded offerings in genetics, diagnostics, digital tools and data analytics.

Zoetis has a disciplined approach to research and development and partners extensively with veterinary schools, academic institutions and clinical practitioners. This ecosystem is designed to generate insights that are both scientifically rigorous and commercially relevant. A collaborative approach has helped Zoetis consistently lead key therapeutic categories, including the development of the first COVID vaccine for animals.

Consequently, Zoetis has outperformed the broader animal health market. Over the 12 years to 2025, revenue grew at an average of 8% per year, compared to 5% for the wider industry. Since listing, earnings have grown at an impressive 13% per year on average.

The pet economy

Zoetis has been a major beneficiary of the structural rise in pet ownership, underpinned by three durable forces.

First, the increasing humanisation of pets. A recent US study found that 9 in 10 dog owners value their dog's health as much as, or more than, their own. This sentiment is particularly strong among Gen Z. With nearly two-thirds of US households owning at least one pet, powerful commercial tailwinds continue to build.

Second, companion animal lifespans have lengthened materially due to advances in nutrition and veterinary care. Dogs lived an average of nine years in the 1980s. Today, that figure is closer to 13 years. Cats have moved from 7 years to around 12. Longer lifespans lead to more frequent vet visits, increased medication use and a greater demand for treatments as age-related conditions (ie tumours, parasites, and arthritis) become more prevalent.

Third, spending on pets has proven resilient through economic cycles. When household budgets tighten, 70% of owners would rather cancel streaming subscriptions and 91% would spend less on dining out, before reducing pet spend. Zoetis’ research suggests that 86% of owners would pay

“whatever it takes” for essential pet healthcare.

The company’s increasing focus on companion animals (now 65% of sales) reflects this dynamic. Pet owners tend to make decisions more emotionally than economically, supporting higher innovation uptake and stronger margins than livestock markets, where farmers apply stricter cost-benefit criteria.

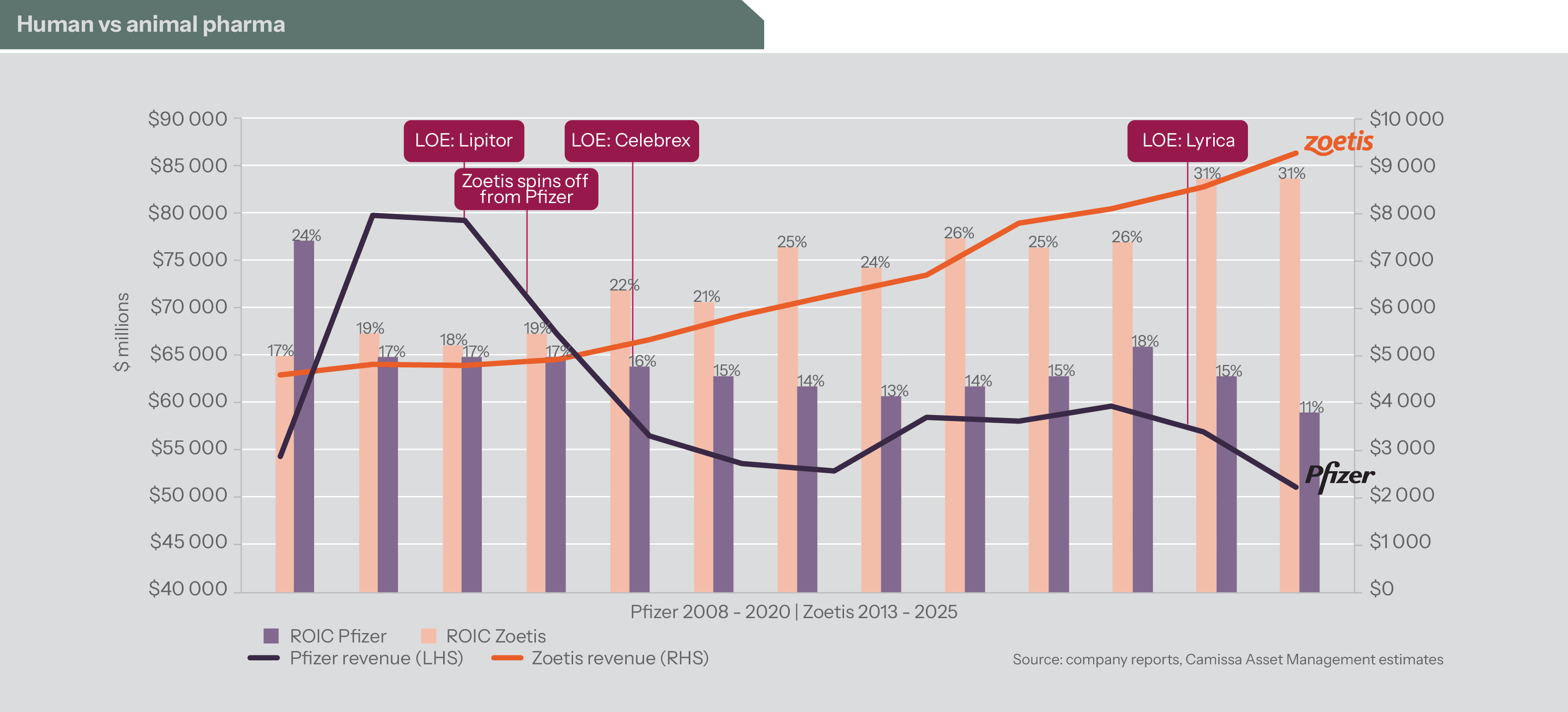

Human versus animal pharma

The animal health market benefits from several structural advantages over the human pharmaceutical market. Research and development timelines are shorter (around 7 years versus 12–15 years for human pharma) and costs are materially lower, while still meeting stringent standards. Smaller, faster-enrolling trial populations further accelerate development.

In addition, success rates are around four times higher. Many animal drugs are adaptations of compounds already proven in other species, significantly reducing risk in development. A molecule validated in dogs, for example, can often be reformulated for cats with relatively limited additional investment.

Perhaps the most important advantage relative to the human drug industry is the absence of dominant third-party payers. Human pharma must contend with insurers and government formularies that compress pricing. In animal health, the paying customer is usually the pet owner, guided by their vet. Patent protection also tends to be more durable: while generics exist, smaller market sizes deter widespread generic provider entry and vet-driven brand loyalty creates a lasting competitive moat.

Together, these dynamics enable Zoetis to commercialise innovation efficiently, delivering high financial returns with lower structural risk. By contrast, human pharma companies (such as Pfizer) typically face sharp revenue declines when blockbuster drugs experience loss-of-exclusivity (LOE), alongside a weaker return on invested capital (ROIC) profile - see chart below.

The chasing pack

While Zoetis remains the clear leader, rivals Elanco and Merck Animal Health, have introduced competing products across key categories. Credelio (Elanco) and Bravecto (Merck) challenge Simparica Trio in parasiticides, while Elanco’s Zenrelia and Merck's Numelvi target Zoetis’ Apoquel in dermatology. Elanco's aggressive promotional pricing of Zenrelia has led to market share losses for Zoetis, with Numelvi's recent approval adding further competitive pressure - though Zoetis is responding with line extensions and improved formulations, consistent with its innovation-led strategy.

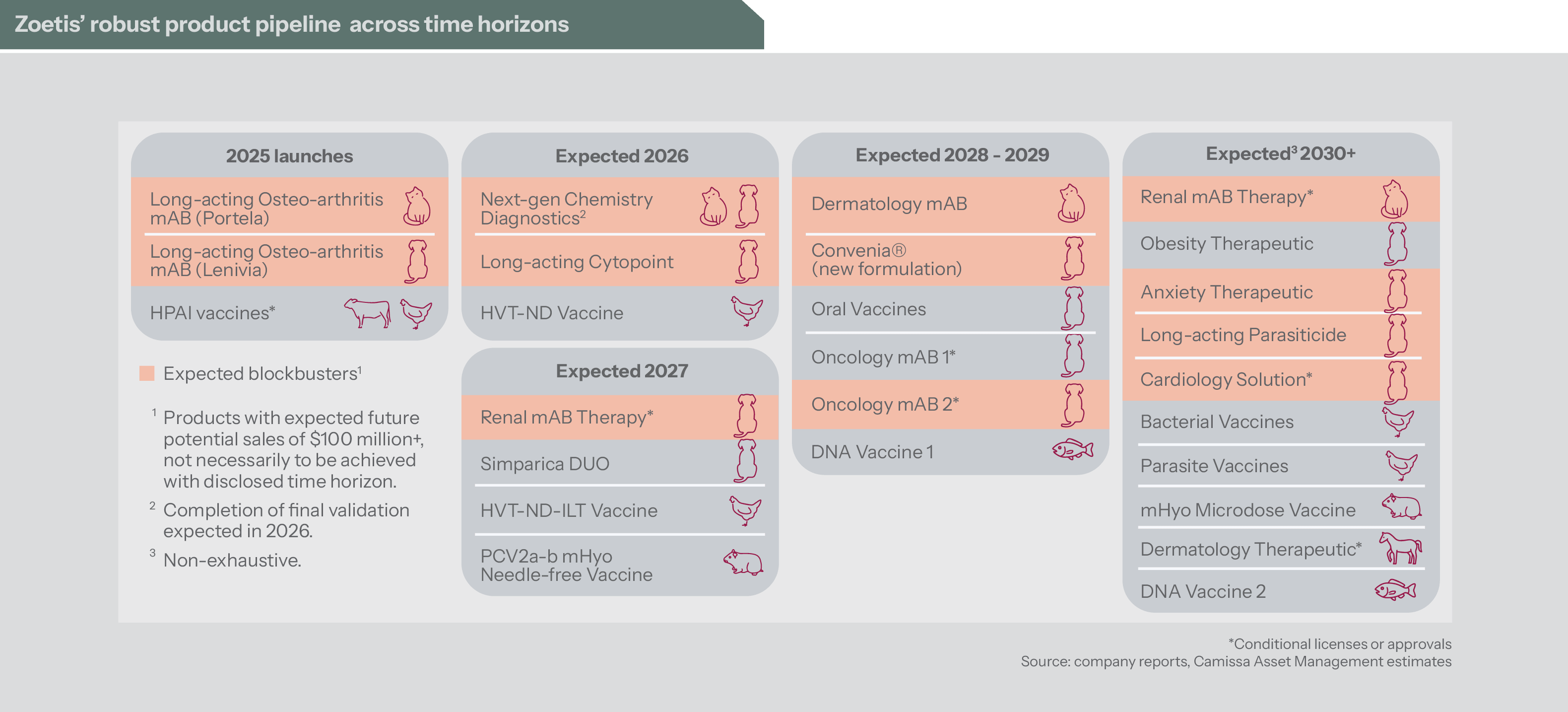

A pipeline with bite

Innovation is central to Zoetis’ long-term growth and the company’s pipeline remains one of its strongest assets. Major product launches are planned annually over the next several years (tabled below), with chronic kidney disease - the leading cause of feline mortality - being a key area of focus. Zoetis has seven drugs in development that target this condition in an estimated $3-4 billion per annum market with no disease-modifying treatments currently available.

Oncology is a strategic priority, with Zoetis developing purpose-built therapies specifically for canine cancers. Cancer affects one in four dogs and one in five cats and it remains the leading cause of death in adult dogs (accounting for over 30% of US cases). Despite this, treatment options are limited and largely repurposed from human medicine.

Altogether, new therapeutic areas represent more than $5 billion per annum in opportunity - significant relative to current Zoetis revenue of $9.5 billion per annum.

The pipeline also reflects a deliberate shift toward greater complexity, with increasing investment in monoclonal antibody (mAb) technologies. Unlike conventional synthetic drugs, these biologics are derived from living organisms and target specific biological pathways with precision. Despite higher development costs, they offer stronger efficacy and transformative potential across cancer, allergies, diabetes and osteoarthritis pain.

A leader in a growing market

Zoetis stands as the leader in a structurally growing market, supported by rising pet ownership, ongoing pet humanisation and resilient owner spending. Its innovation-led culture, enduring vet relationships and differentiated pipeline position it for above-market growth over the long term. Despite the competitive headwinds, we view the recent share price weakness as a compelling opportunity to hold this exceptional business in our clients' portfolios.