SA gambling: the house goes mobile

Online gambling has surged in South Africa over the past five years, overtaking all other forms to become the country’s largest gambling channel. This shift has reshaped the industry’s structure and competitive dynamics. Operators are increasingly prioritising online platforms to capture growth, while protecting profitability by improving operational efficiency and optimising their mature, land-based portfolios.

We outline the key South African gambling segments, examine the economics of different gambling formats and analyse the drivers of the rapid growth in online gambling, while considering international market evolution and how domestic operators are adapting their strategies.

Gambling market structure and segmentation

South Africa's gambling market is primarily segmented by regulation, with each category operating under distinct licensing frameworks and economic characteristics. The main regulated segments are:

- Land-based casinos: physical venues licensed to offer slot machines and table-based games such as blackjack, poker and roulette. They are typically large-scale, capital-intensive properties and have historically been the dominant gambling format in the country.

- Bingo: offered through electronic terminals located in dedicated venues, often shopping centres. While the underlying game remains traditional bingo, electronic terminals automate gameplay and number matching, making the experience faster and easier to follow.

- Limited payout machines (LPMs): similar in appearance and gameplay to casino slot machines but these are limited by regulatory caps on the size of permitted bets and payouts. They are commonly located in pubs and bars and designed to offer low-stakes gambling, with a maximum bet of R5 and a maximum payout of R500 per game.

- Bookmakers: licensed to accept bets at fixed odds on the outcome of an event, most commonly with sporting matches and horse racing. The odds agreed at the time of placing a bet determine the potential payout.

- The National Lottery: operates separately from other gambling formats and is regulated under its own legislation. Players purchase tickets and select numbers, with prizes based on the outcome of scheduled draws.

- Online platforms: offer an additional distribution channel through which players can access casino-style games and sports betting. While the underlying activities are regulated, the digital channel has fundamentally changed how and where players engage with gambling products.

Bringing the house to the consumer

The expansion of online gambling has materially increased the size and relative importance of the digital channel within South Africa’s gambling market (shown below). In the year to 31 March 2020, total gross gaming revenue (excluding The National Lottery) amounted to R32.7 billion, of which online gambling contributed R8.8 billion (27%). By 31 March 2025, total gross gaming revenue had risen to R74.5 billion, with online gambling accounting for R52 billion (70%).

COVID was a key catalyst for this acceleration as lockdown restrictions made online platforms the only accessible option. During this time, regulatory acquiescence to operators’ interpretation of existing laws extended the use of bookmaker licenses for online gambling. Many players who migrated online during lockdown have continued using these platforms. This is mainly because physical gambling formats have faced additional challenges, such as loadshedding and related safety concerns, which have reduced evening footfall across all segments.

Beyond the pandemic, online gambling offers structural advantages in convenience and accessibility, as players can participate from home at any time, eliminating travel costs and time constraints. In addition, new game formats (eg crash games) are only available online, further enhancing the appeal of this channel.

Importantly, online gambling has taken market share from physical gambling formats and is expanding the overall market by attracting new players. Moreover, whereas traditional formats such as casinos, bingo and LPMs have historically attracted an older customer base, online gambling is appealing to younger players with greater digital familiarity, who were previously underrepresented in physical gambling venues.

The economics of gambling formats

Online gambling currently generates lower cash operating margins (typically around 20-25%) than established physical formats. Large land-based casinos tend to achieve margins of around 35%. This reflects the higher level of online competition with lower geographic moats and elevated marketing and bonusing costs, which constrain profitability.

Operators must continually invest in online infrastructure to ensure intuitive navigation, attractive design and uninterrupted gameplay. They must also offer reliable payment systems, which is particularly important as it underpins trust and confidence between users and operators. Yet despite these investment requirements, online gambling remains less capital intensive than land-based formats. Physical casinos require substantial ongoing capital expenditure to maintain and refurbish their premises and gaming assets - such as tables, slots, bingo terminals and LPMs.

Conversely, marketing and customer acquisition costs are higher online, with bonusing playing a central role. Bonuses allow newer players to wager without risking their own capital, to encourage trial and long-term engagement. As competition has intensified, marketing and bonusing spend has increased, raising acquisition costs. In response, operators are focusing on scaling their platforms to improve operating leverage and support reinvestment in growth.

International market dynamics

In the nascent US online gambling market, Flutter (operating as FanDuel) and DraftKings are two of the largest competitors. As states legalised online gambling, these operators aggressively marketed their platforms and offered frequent bonuses to rapidly acquire players. Despite strong revenue growth, operators initially generated cash operating losses. This prompted operators to prioritise customer lifetime value, with higher engagement - characterised by more frequent and higher-value bets - improving returns on marketing and promotional incentives. Although revenue from a growing base of active players is being reinvested in marketing to attract additional players, this has become increasingly costly as competition has intensified. As shown below, further to reaching high market shares and growing customer lifetime value, Flutter and DraftKings recently achieved modest cash operating profits.

Flutter, along with operators like Evoke and Betsson, also operate in mature markets (i the UK and Italy). Here, player acquisition has slowed, competition is more concentrated and operators prioritise user retention and increasing share of players’ total gambling spend. Cash operating margins have stabilised at around 25% and marketing spend as a percentage of revenue has declined with scale. Smaller operators that are unable to scale and generate sufficient cash flow for reinvestment have exited these markets.

SA operators’ strategic adaptation

Hollywoodbets and Betway are the two largest online gambling operators in South Africa and together are estimated to account for more than 50% of the market. They entered the online sports betting market early, affording them the time to build trusted brands and a technological infrastructure that now supports their online casino-style games.

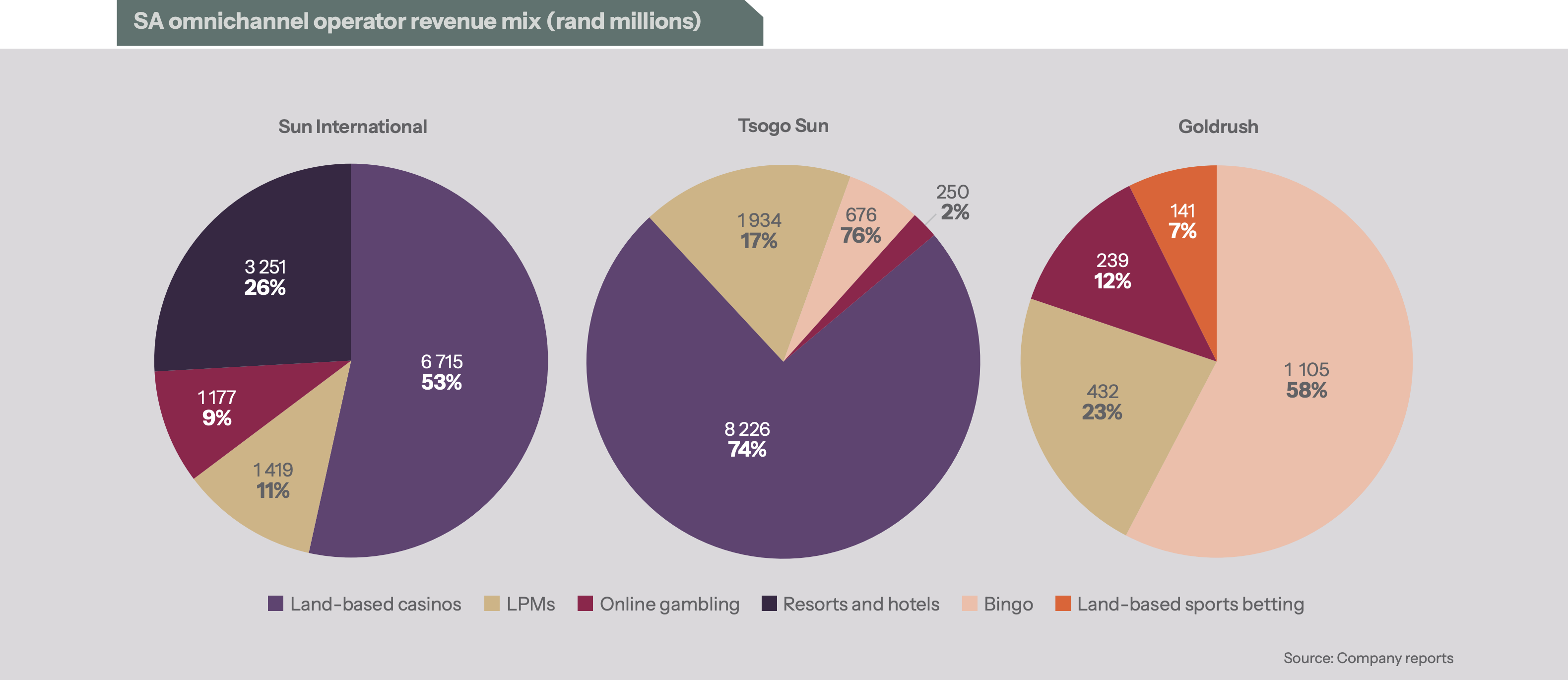

Given the structural change in the South African gambling market and the proliferation of competition, operators with established physical footprints are adapting by developing online platforms to participate in the sector’s fastest-growing channel. Groups such as Sun International, Tsogo Sun and Goldrush are pursuing omni-channel strategies that integrate digital and physical offerings. Key to this approach is the introduction of unified customer wallets, allowing players to use a single balance across online and land-based channels. Unified loyalty programmes further deepen engagement by enabling the redemption of online-earned rewards at physical casino precincts, including hotels and entertainment venues.

Online platforms also provide operators with valuable customer data, delivering deeper insight into player behaviour, more targeted marketing and improved engagement, while reducing inefficiencies in bonus and promotional activity. Among the land-based, listed operators, Sun International (Sunbet) has progressed most rapidly, commanding roughly 3% of the market, with online revenue significantly larger than that of Tsogo Sun (playTSOGO) and Goldrush (Gbets) - illustrated below. Both competitors are investing in skills, technology and marketing, which should support faster scaling over time and enable them to expand their market shares beyond the current 1%. Evolution in international markets has shown that this is essential to remain competitive in the long term.

Within weakening physical channels, operators are focusing on cost control and footprint optimisation. This includes reducing machine counts to improve utilisation, relocating machines to higher-performing sites, and disposing of smaller or underperforming casinos. Despite the rapid expansion of online gambling, large urban land-based casinos have demonstrated resilience as entertainment hubs, continuing to generate strong cash flows.

Omnichannel strategy bodes well for investors

Online gambling continues to expand in South Africa, reshaping the industry and attracting new customer segments. While Tsogo Sun and Goldrush have been slower to scale their online platforms, ongoing investment positions them to participate more meaningfully in future growth. Given their late start and the scale of established online operators, the three listed gambling companies are unlikely to gain meaningful market share. However, online gambling will be a source of growth and their traditional gambling businesses are inexpensively priced on the stock market today.