GTT powers liquefied natural gas growth

Few companies can claim to have designed the invisible infrastructure underpinning an entire global industry. Gaztransport & Technigaz SA, a French engineering company headquartered in the quiet Parisian suburb of Saint-Rémy-lès-Chevreuse, with just 738 employees, is one such company.

Trading as GTT, it commands over 90% market share in the design of membrane containment systems for liquefied natural gas (LNG) carriers - an almost monopolistic position that should attract any investor focused on competitive moats. We investigate the technology, market position and exceptional economics behind this low-profile firm.

Innovation to integration

GTT’s roots stretch back to the early 1960s, when European engineers met the challenge of transporting Algerian natural gas across the Mediterranean. The idea of a pipeline was abandoned due to regional instability, prompting innovators to develop a way to ship gas in liquid form at cryogenic temperatures of minus 163°C. Two French companies emerged from this effort:

Technigaz, founded in 1963 as a subsidiary of Gazocean (a joint venture between Gaz de France and Japan’s NYK Line), patented membrane containment panels in 1964. It delivered its first LNG carrier the same year.

Gaztransport SA, established by the Worms Group in 1966, followed with the competing Invar steel containment system. Its first vessel, the Polar Alaska, was delivered in 1969.

For three decades, these rival firms independently refined their cryogenic membrane technologies amid a turbulent LNG market, including the industry downturn of the 1980s. In 1994, they merged to form Gaztransport & Technigaz, uniting their complementary Mark and NO containment systems. The new entity was initially owned by Gaz de France (40%), Total (30%) and Bouygues Offshore (30%). In February 2014, GTT listed on the Euronext Paris in an IPO that underscored the strength of its competitive position.

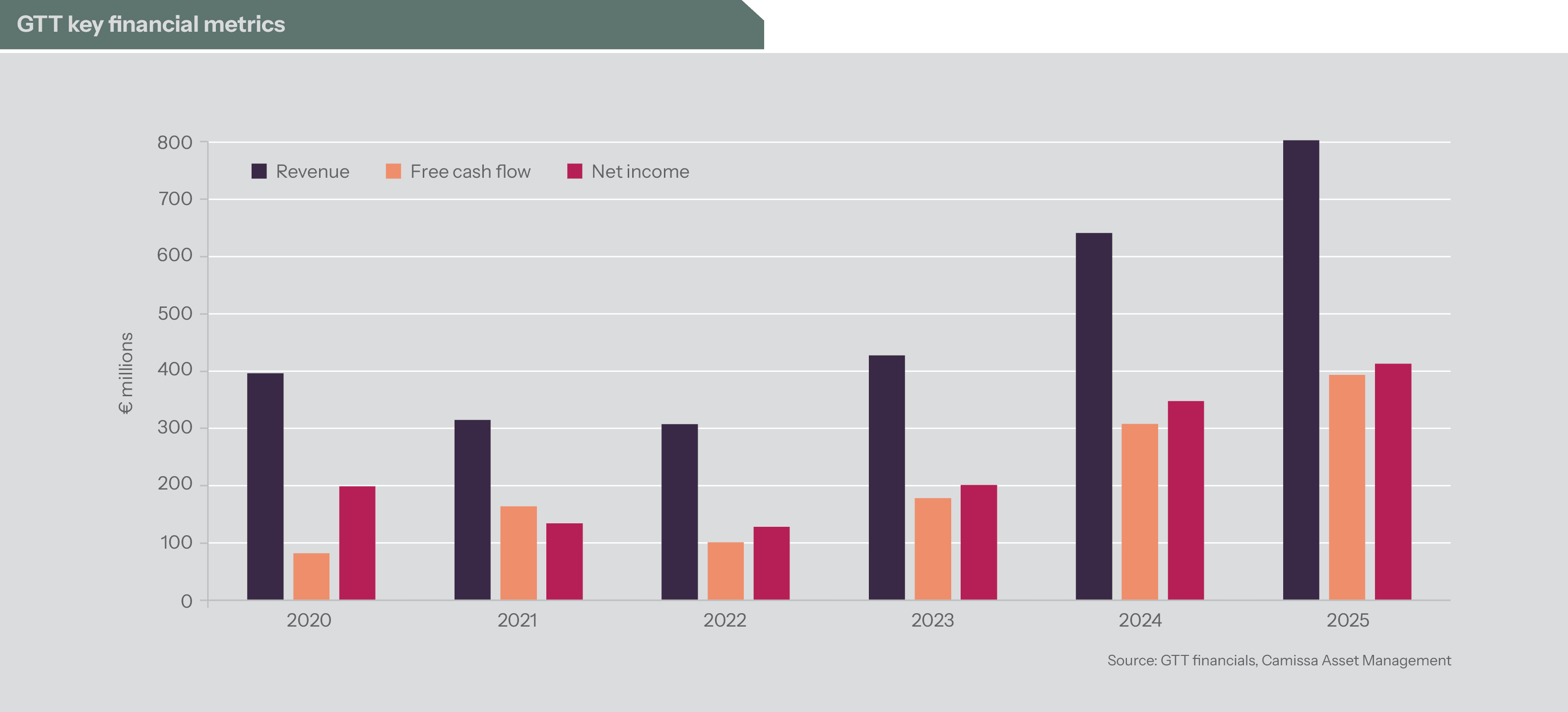

In 2024, GTT posted record revenue of €641 million, up 50% from the year before, and an operating profit margin exceeding 60%. These are remarkably strong metrics.

Exceptional economics

GTT operates an asset-light licensing model, designing containment systems and licensing the technology to shipyards. It earns royalties on each vessel built.

This technology is installed on more than 80% of the global LNG fleet. Nearly every new carrier constructed in the world’s leading Korean and Chinese shipyards carries a GTT license.

The business model has an exceptionally lean cost structure, with gross margins consistently exceeding 95%, while operating profit margins have held between 50% and 55% over the past five years. GTT’s financial performance reflects the cyclical nature of LNG carrier orders, which softened in 2021–2022 before rebounding to record levels in 2025.

Revenue more than doubled from €307 million in 2022 to €803 million in 2025, with earnings rising to €413 million and free cash flow reaching €393 million, as charted below. The company ended 2025 with €218 million in net cash.

Fuelling growth, managing risk

The investment case for GTT rests on expanding global LNG demand, which is currently propelled by several converging forces:

- Energy security concerns have prompted European and Asian countries to diversify gas supply through adding long-term LNG contracts.

- Environmental regulations from the International Maritime Organisation are pushing the shipping industry to adopt LNG as a marine fuel, creating additional demand for GTT’s fuel tank designs.

- Record new liquefaction capacity is coming online, necessitating a corresponding wave of new carrier orders.

- An ageing LNG fleet, with many vessels over 25 years old, adds a further replacement-driven demand tailwind.

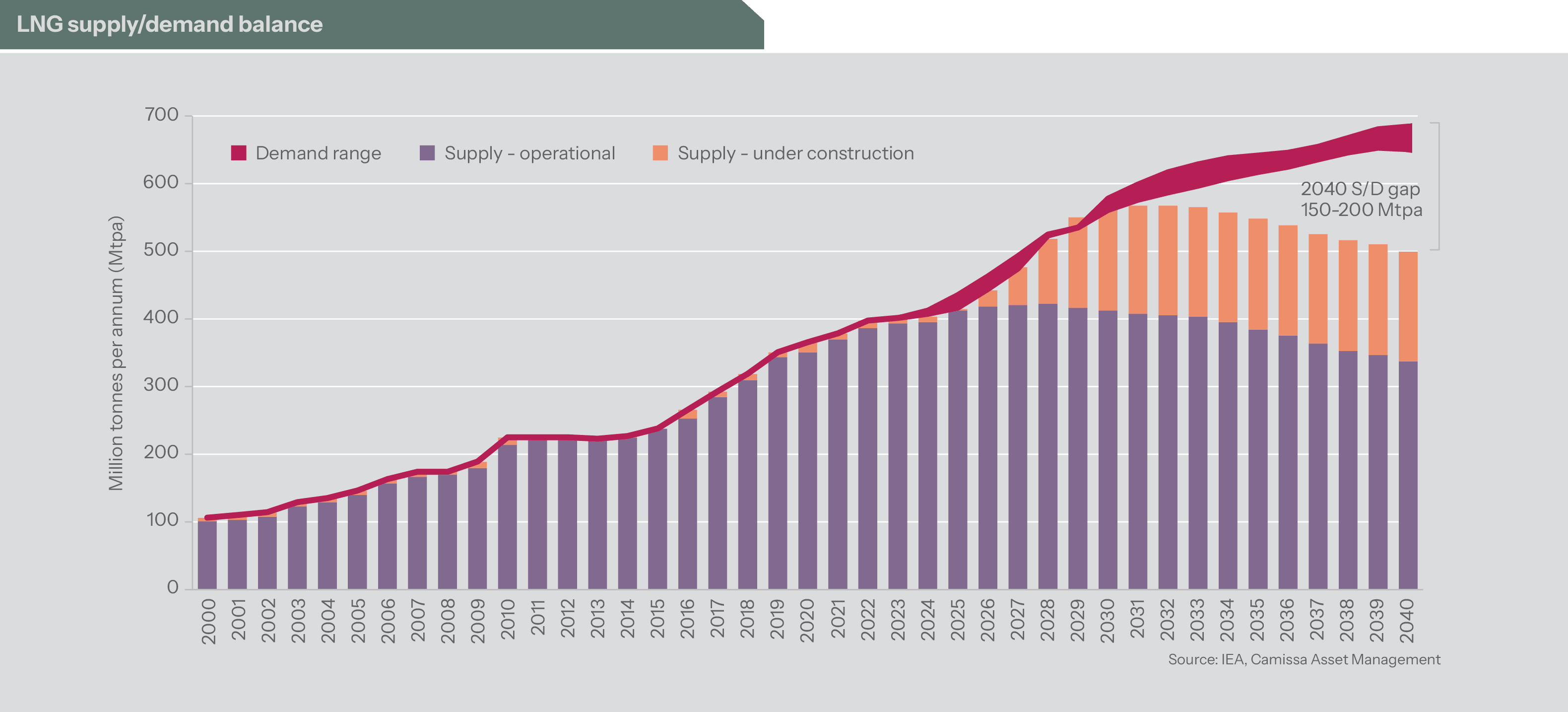

Below, we highlight the outlook for LNG supply and demand as forecast by the International Energy Agency (IEA). The IEA projects a growing shortfall in supply that is likely to peak at around 200 million tonnes by 2040 based on its forecast of demand growth and current operational LNG supply, as well as new LNG supply under construction.

There are, however, risks to these forecasts. Geopolitical conflicts and US tariff changes have introduced caution among shipowners in timing orders.

Additionally, Korean shipyards, GTT’s primary customers, have developed competing containment technologies (including KOGAS’s KC-1 and Samsung’s KCS systems), yet none match GTT’s proven track record.

Finally, the long-term trajectory of global decarbonisation raises questions about the duration of LNG’s role as a transition fuel, though forecasts point to sustained robust demand for at least the next two decades.

Competitive advantages and barriers to entry

GTT’s competitive moat is among the widest in industrial engineering. At the end of 2024, it held 3 482 active worldwide patents and ranked first among French mid-cap companies for patent filings at the National Institute of Industrial Property for four consecutive years. Its Mark III Flex+ and NO96 Super+ systems cut boil-off rates to just 0.07% of cargo per day. This is roughly half that of competing Korean alternatives. This directly lowers fuel costs and emissions for shipowners. Additionally, the certification process with international classification societies (Bureau Veritas, Lloyd’s Register and DNV) is lengthy and rigorous, creating a formidable qualification barrier for new entrants.

Beyond technology, GTT enjoys deep, long-standing relationships with the three major Korean shipyards (HD Hyundai, Samsung Heavy Industries, Hanwha Ocean) and China’s Hudong-Zhonghua, which together build most of the world’s LNG carriers. Switching costs are high as shipyards have invested for decades in tooling, training and workflow integration with GTT’s systems. The royalty-based model eliminates manufacturing risk and gives the company significant operating leverage, whereby incremental revenue flows almost entirely to the bottom line.

Order book visibility

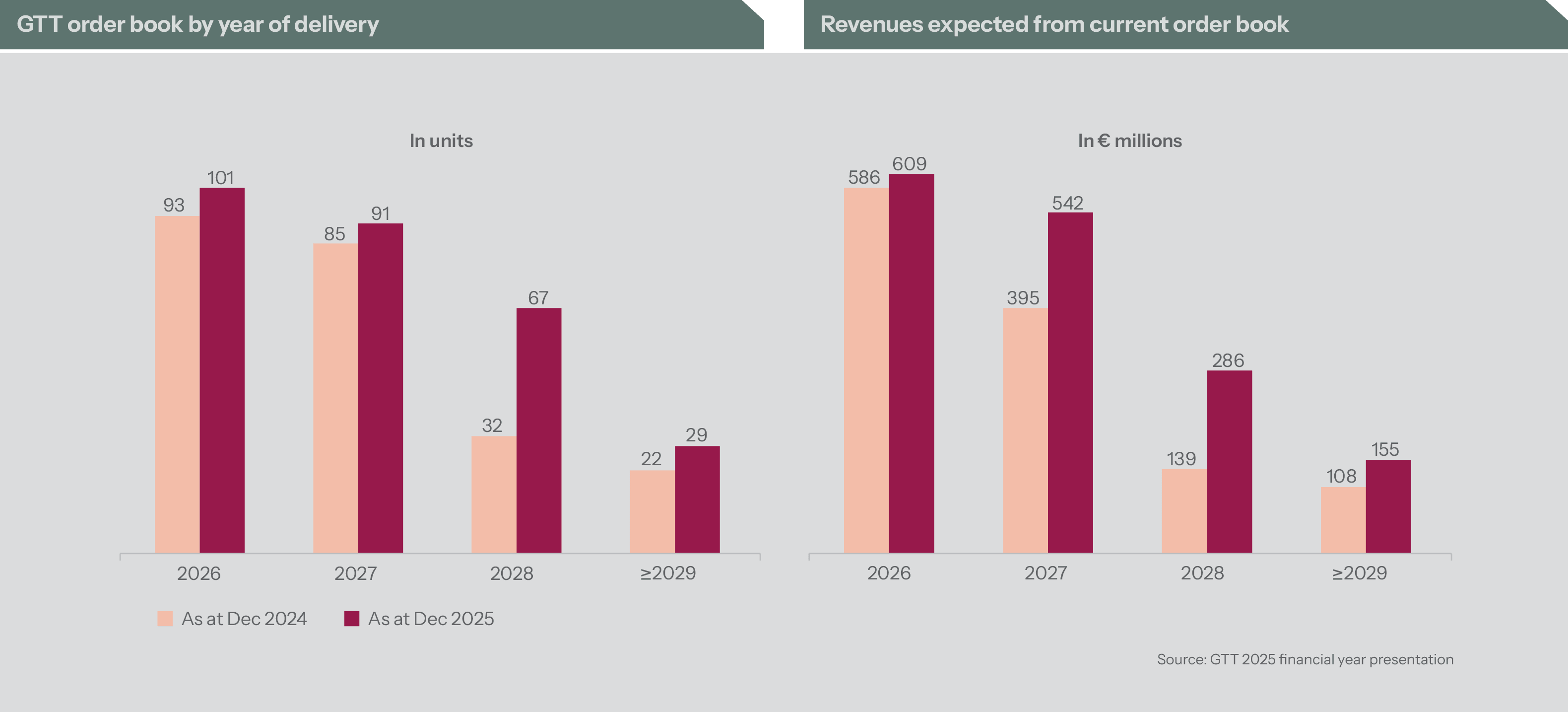

As shown below, GTT’s order book totalled around €1.6 billion across 288 units at the end of 2025, providing multi-year revenue visibility. Management expects 150 new LNG carrier orders in 2026, supported by the record wave of US LNG project approvals and ongoing fleet replacement needs.

The strength of specialised intellectual property

GTT is that rarest of industrial enterprises: a capital-light technology licensor with monopoly-like market share, extraordinary margins, a fortress balance sheet and a multi-decade structural growth runway. Its containment systems are the critical enabling technology for the global LNG market, which is expanding as the world navigates the complex transition from coal to cleaner fuels. While geopolitical crosscurrents and nascent Korean competition warrant monitoring, GTT’s 60-year head start in cryogenic engineering, its unmatched patent portfolio and deeply entrenched relationships with the world’s shipyards make it an exceedingly difficult franchise to replicate.

With a €1.6 billion order book providing visibility to the end of the decade, record earnings momentum and emerging optionality in hydrogen and ammonia transport, GTT presents a compelling investment case. The enduring power of its specialised intellectual property produces superior economic results, which are benefiting our clients.