Carrier's growth transition for a warming world

Carrier Global (Carrier) manufactures heating and cooling products for residential homes, commercial buildings (including data centres) and cold chain transportation. The company was founded in 1915 in New York City by Willis Carrier who invented modern air conditioning in 1902. Carrier has since evolved from a traditional air conditioning company, into an innovative global leader in temperature control solutions.

We unpack Carrier’s business model, the cooling off of American residential market demand following a boom, the company’s strategic expansion into Europe and the high-growth opportunities from data centre cooling and aftermarket services.

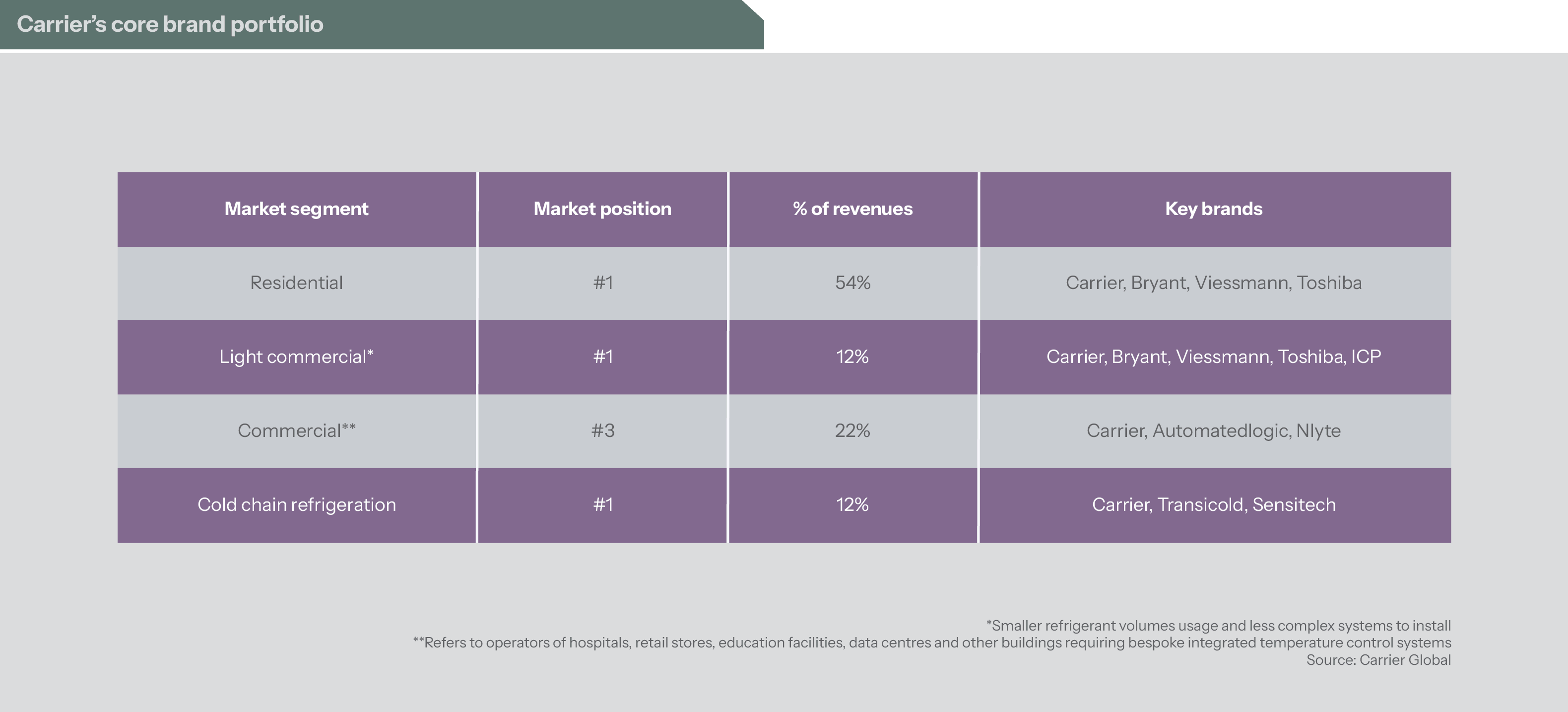

Carrier’s key brands

The table below highlights Carrier’s core brands across market segments, along with their positioning. Its key market-leading brands include:

- Carrier - the dominant brand in the Americas;

- Viessmann - a top-tier player in Europe; and

- Toshiba – a premium brand in the Asia-Pacific region.

Carrier’s US market post-boom

North America remains Carrier’s core market, where it holds the leading market share with a large installed product base and deep penetration within dealer and independent installer networks.

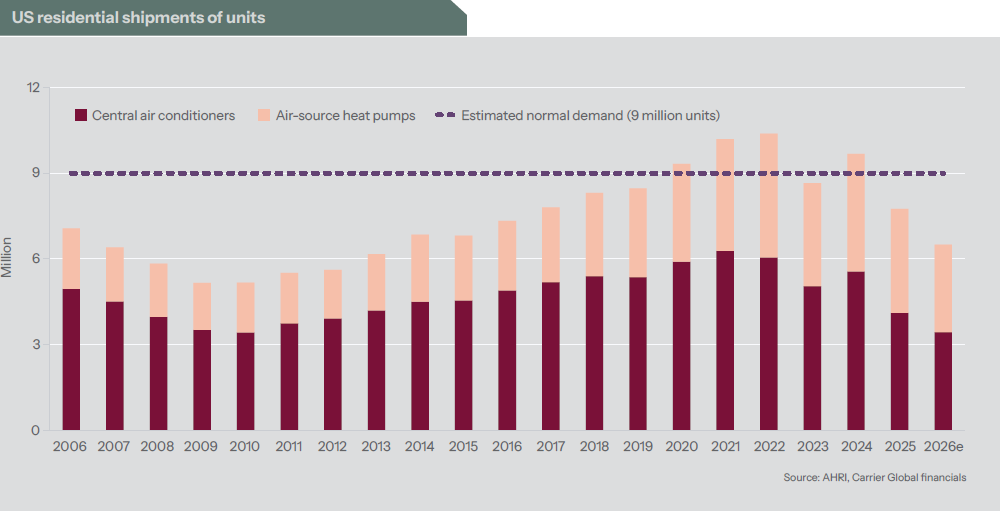

The US residential market experienced a period of surging demand following the 2020 pandemic - charted below. The shift to working from home, combined with subsidies from the Inflation Reduction Act (IRA) and the prevailing low interest rates, accelerated the replacement cycle for home heating and cooling products. However, by the end of 2025, these pandemic-era tailwinds had abated. The demand for air conditioning units and air-source heat pumps has subsequently declined and is expected to contract further in 2026.

The US market is predominantly driven by replacement demand, with 75% of new unit sales replacing legacy systems. Old air conditioners are significantly more energy-intensive than modern units due to outdated technology, worn components and lower efficiency - often consuming twice the energy to achieve the same effect. Upgrading to modern systems can yield material long-term electricity cost savings that more than justify the conversion costs.

Looking ahead, industry volumes are poised to resume growth as a vast portion of the aging, inefficient residential units are replaced. This cycle is expected to gain momentum through 2027 and beyond. In this consolidated1 residential market, Carrier’s incumbent brand and dominant distribution footprint position it well to capture the forecasted growth.

1 The top 10 companies in the USA’s air conditioner market account for over 80% of sales.

Positioned for the EU’s energy transition

Carrier’s European business primarily serves the need for indoor heating rather than air conditioning. Its recently acquired Viessmann business is the leading German provider of integrated home energy management systems, encompassing heat pumps, solar panels, battery storage and smart thermostats.

Following the cancellation of fossil-fuel boiler subsidies in early 2025, the market is transitioning from legacy gas boilers to high-efficiency electric heat pumps, which are four times more profitable for Carrier than gas boilers.

While the upfront cost of a heat pump remains higher than a boiler - a factor that initially tempered the transition - robust government support in key markets like Germany, UK, France and Italy has mitigated this barrier. In Germany, which accounts for half of Viessmann’s revenue, government subsidies can cover up to 70% of installation costs for compliant heat pump systems. Post-installation, electric heat pumps deliver significantly lower operational expenses than traditional gas boilers, while drastically reducing carbon emissions, particularly when the electricity comes from renewable sources.

Data center cooling

Perhaps the most explosive area of growth for Carrier is data centre cooling. The rapid progress in, and utilisation of, artificial intelligence (AI) systems has resulted in enormous growth in the building of new data centres, and plans for future builds are exponentially larger. High-density AI server racks operating at peak utilisation can reach internal temperatures of between 85°C and 95°C and require uninterrupted cooling. This structural demand has seen Carrier’s data centre revenue double between 2024 and 2025.

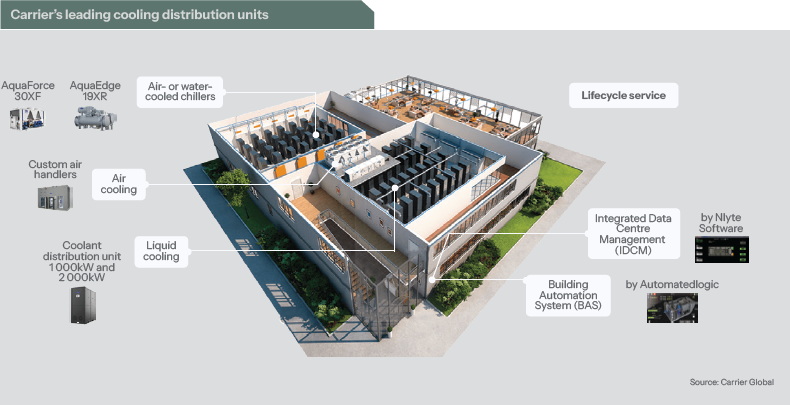

While legacy data centre architectures rely heavily on traditional air-cooling chillers, which currently comprise 87% of the market, next-generation AI racks require direct-to-chip liquid cooling. Carrier is actively innovating to provide for this shift, with advanced Coolant Distribution Units (CDUs) that sit adjacent to servers to continuously circulate low-temperature, non-conductive coolant directly over the chips – as illustrated below.

Carrier provides a fully integrated, customised ecosystem, which includes hardware (chillers, air handlers and CDUs) and specialised software (building automation systems and dedicated engineering services within close proximity). This comprehensive, full-system offering creates high switching costs for clients and differentiates Carrier from component-only manufacturers.

Building a high-margin service network

Historically, 75% of Carrier products were serviced by third-party providers or in-house teams rather than Carrier itself. Since 2020, management fundamentally shifted strategy to transform after-sales into a core operational pillar to capture lucrative, recurring revenue streams. Aftermarket sales have grown by 15% per year since then, representing around 23% of total group revenue in 2025.

In its Commercial division, Carrier currently has an installed base of over 400 000 chillers, yet fewer than 60% are serviced by the company. As these systems become more complex, in-house and independent maintenance teams are struggling to keep pace with the technical expertise of Carrier’s specialised own technicians. This represents a substantial growth opportunity for Carrier to convert un-serviced units into long-term service agreements. By capturing these high-margin after-sales contracts, Carrier secures recurring revenues.

To sustain and further this shift to providing after-sales servicing, Carrier is pursuing structured initiatives in its main markets. In the US, the Techvantage program aims to address the skilled labour deficit by hiring 1 000 new technicians and training 100 000 more by 2030. In Europe, the System Profi program is actively upskilling Viessmann’s 80 000 installer partners into ‘System Installers’ capable of generating five times more revenue than traditional single-product installers.

Transitioning for growth

Carrier is pivoting from a pure hardware seller to an integrated temperature control solutions provider, thereby accelerating growth and boosting profitability. The company’s revenue growth will be primarily driven by the product transition toward decarbonisation, demand for AI data centre infrastructure cooling, and the expanding provision of high-margin services. Consequently, in a world of increasingly extreme temperatures due to climate change, Carrier presents a compelling investment case for clients in our global funds.