Governments borrow to fund their fiscal deficit, that is any shortfall from their tax revenue received relative to their expenditure incurred, primarily by issuing debt securities to the private sector. These sovereign bonds have a variety of terms to maturity, from months ahead to many decades into the future, and may have interest rates that are fixed, floating or linked to a fixed real rate over future realised inflation.

We focus on fixed-rate long bonds and assess the appropriateness of the current market pricing of the part of their yield that compensates investors for taking on South African government long-term credit risk.

Decomposing fixed-rate bond yields

Prospective yields to maturity of fixed rate government bonds may be decomposed into three components: (i) a risk-free rate, (ii) a sovereign credit risk premium – the additional premium in the rate that is compensation for taking on the relevant country’s government credit risk, and (iii) the currency risk premium1, which compensates investors for the risks stemming from the fact that the loans are denominated in the currency of the borrowing country.

1The currency risk premium attempts to price for the expected loss of purchasing power of the currency relative to liquid, stable developed economy currencies, and the risk of potential variability around these expectations (ie the expected inflation differential and a premium for the variability of this differential).

Current market pricing of the South African credit risk premium

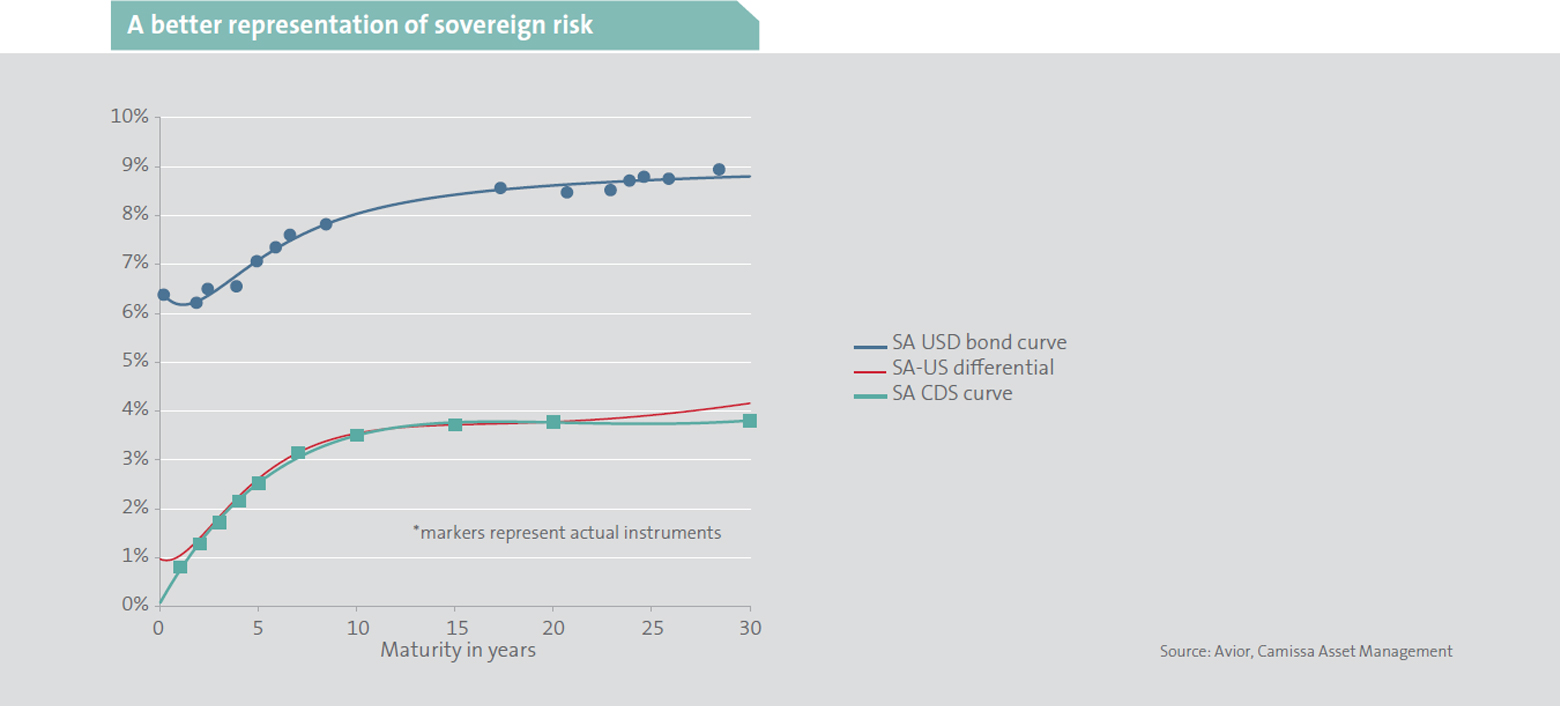

Sovereign credit risk relates to the issuing government’s ability to meet their debt obligations, interest and principal, over the term of the borrowing. To simplify the analysis, we assume that US government bonds issued in US dollars (US Treasuries) represent a risk-free alternative and therefore, the SA credit risk premium is the excess yield of a US dollar-denominated SA government bond over the equivalent term US Treasury. The additional risks posed by the rand currency are eliminated by comparing bonds both issued in dollars. South Africa currently has 15 US dollar-denominated bonds in issue, ranging in maturity from 2024 to 2052. These bonds are exchange-traded, liquid and exhibit transparent pricing and available data on value traded.

An alternative measure of the South African credit risk premium is the price of a credit default swap (CDS), which is a derivative instrument used to mitigate such risk by transferring the credit risk from the debt holder to the counterparty of the CDS (ie effectively the price of insuring against a South African government default in dollars). Credit default swaps are traded over the counter directly between two parties. CDS instruments exhibit less liquidity (than equivalent term SA dollar bonds) for maturities longer than 10 years and are consequently less reliable pricing indicators beyond 10 years to maturity.

The chart below shows that current market pricing of South Africa’s credit risk premium is similar between the bond differential and CDS spreads, except at longer durations. Given the greater market liquidity in the former, the gradual upward slope in the credit risk premium (implied by the bond differential) seems the more accurate market price at this stage. This risk premium rises from around 1% pa at the short end, to about 3% pa from five years out, and then to around 4% pa for longer terms to maturity2.

2Strictly speaking, this rise beyond a 20-year term is due to the counterintuitive fact that, currently, the US yield curve declines after 20 years (ie a 30-year Treasury yields less than a20-year comparative bond).

South Africa’s sovereign rating

Sovereign credit risk is assessed through an analysis of various country-specific criteria including economic outlook, political stability, fiscal position and the strength of a country’s legal and financial regulatory framework.

Moody’s, Standard & Poors (S&P) and Fitch are the three most influential rating agencies that assess sovereign creditworthiness. Currently, all three agencies have assessed South Africa’s sovereign rating as below investment grade, with a stable outlook. The trajectory of ratings has been negative over the last few years as South Africa’s fiscal position has deteriorated. The drop below investment grade happened in 2020 for Moody’s and 2017 for S&P and Fitch.

Concentrating specifically on the Moody’s rating framework in this analysis, its’ country rating is built up from sub-factors. These include ratings and assessments for economic strength and resiliency, institutional strength, depth of capital markets, offshore liabilities, banking and political risks and fiscal strength (the most important component).

According to Moodys’ assessment, the overall country rating is two notches below investment grade. Importantly, all sub-category ratings for South Africa are above investment grade, a notable positive, relative to comparable countries – except for the fiscal strength sub-category rating, which is five notches below investment grade and clearly the major credit risk issue for the country. Increasing risks to the government debt level and debt affordability metrics are key concerns to the agency and evidently South Africa’s major weakness at present.

South Africa has both economic and structural strengths. It is a sizable economy with diversified GDP contributors, which implies good economic robustness. The quality of its institutions and governance is assessed as investment grade, with the judiciary system and monetary policy effectiveness as key areas of strength. An example of this would be the South African Reserve Bank, which is technically effective at delivering on its mandate and credibly independent in monetary policy implementation. Additional positive attributes highlighted by Moody’s include having adequate levels of foreign exchange reserves, the low level of external debt, the depth of South African capital markets and the diversification of governments’ lenders – debt is readily raised across banks, insurers, asset managers and non-residents.

An analysis of the country’s fiscal position and how it could evolve is therefore crucial in assessing South Africa’s credit risk premium. To do this, we need to start with the current debt position and then assess how it is likely to evolve, given the probable growth in government income and outlays.

Current position

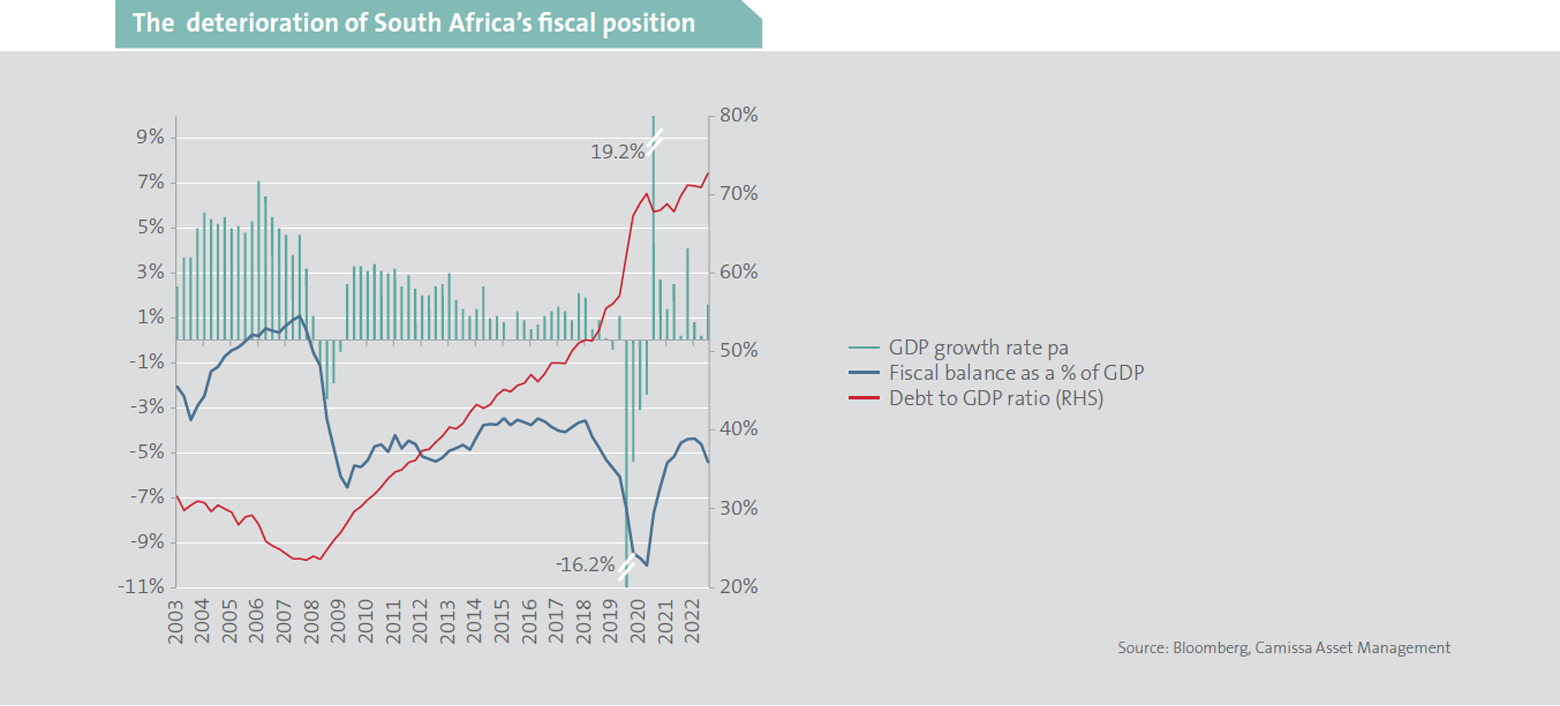

The current debt position relative to the size of the economy, the debt-to-GDP ratio, is currently 72.7%. This is a substantial deterioration from 24% in 2008, when South Africa last ran a fiscal surplus. National Treasury (who have consistently been overly optimistic in their projections) currently forecasts this ratio to peak at 77.7% in 2026 and then decline to 73.6% by 2031. The chart below shows the significant deterioration of the fiscus and economic growth since 2003.

Government revenue outlook

South Africa’s revenue is largely derived from income tax on corporates (20% in 2022) and individuals (35% in 2022), with the third major component being VAT. However, these three categories offer extremely limited scope for increases from tax rate hikes.

Personal income tax rates in South Africa are very progressive and among the highest in the world, tapping a very small proportion of the population. The previous increase to the upper tax bracket from 41% to 45% resulted in lower than anticipated revenue collections. South Africa is therefore arguably at maximum personal tax rates and any further increases would be counterproductive. The tax base is also small and very concentrated with high income earners being material contributors – this base is also declining due to emigration, tax evasion and avoidance.

Corporate tax rates in South Africa are also comparatively very high in the global context. Increases to corporate tax rates will most likely result in lower domestic corporate investment, less direct foreign investment, business closures and relocations. This will therefore ultimately cause negative trends to revenues as South Africa becomes less favourable in which to operate. Increasing corporate tax rates to grow revenues seems unlikely to be a lever that government can pull.

The other meaningful revenue source is VAT. It is a logical taxation source to increase via raising the tax rate, but politically this is not a possibility as it is the one tax that lower income and unemployed South Africans (a vast number of voters) pay. The consequence of a VAT increase would negatively impact the broader population in a country that has a very high unemployment rate of 32.9%.

Government expenditure outlook

Fiscal improvement could also conceivably be achieved by a reduction to government expenditure. The large components of government’s spending are debt servicing costs, public sector wages and social grants. The ability to materially reduce spending in these areas is severely limited. Interest payments, which are a function of rates and debt levels, are contractually immovable.

Social grants similarly cannot be significantly reduced as they are low and meet only the most basic needs of the unemployed, old and poor. Social instability would inevitably arise from reducing this for these people who have nothing else to lose.

The public sector wage bill is very high in a global context, compared to even developed economies that have large public sector service provision to their populations. This is the result of years of wage settlements above those of the private sector and an arguably inefficient use of this work force. These workers are represented by strong unions, who routinely threaten to withhold essential services as a bargaining tool. These workers do provide critical services to the country, such as healthcare, teaching, police and armed forces. While more efficiency and potentially lower future wage increases are possible in a crisis, the reduction in government expenditure from this source is likely to be very slow.

Capital expenditure on infrastructure is another essential government cost. In recent years, the South African government’s allocation to the capital stock of the country has been too low. This is now being revealed by the material inadequacies in the state provision of the country’s energy and logistics needs (acknowledging the most material two). These inadequacies are causing the country to grow vastly below its potential and therefore need to rise in future, rather than be reduced. This is in addition to the vast sums of money the government needs to inject into state-owned companies to achieve their debt sustainability.

The economy has to grow faster

Given the inability to raise tax rates and the inflexibility of government expenditure, the only solution to improve our fiscal position and ultimately improve our credit rating is for the economy to grow faster.

A larger economy, ie higher GDP, would progressively increase the denominator of the debt/GDP ratio, improving this key measure of fiscal strength. Tax revenues would increase without a rise in tax rates as more people are employed, wages rise in real terms and people pay more VAT via increased consumption. Corporates will earn more and consequently pay more tax. If government spending is managed well and more is allocated to infrastructure investment, a self-reinforcing cycle of improving growth will result.

As the country’s fiscal deficit shrinks, government debt balances can be reduced and another virtuous cycle is created as the annual interest burden declines.

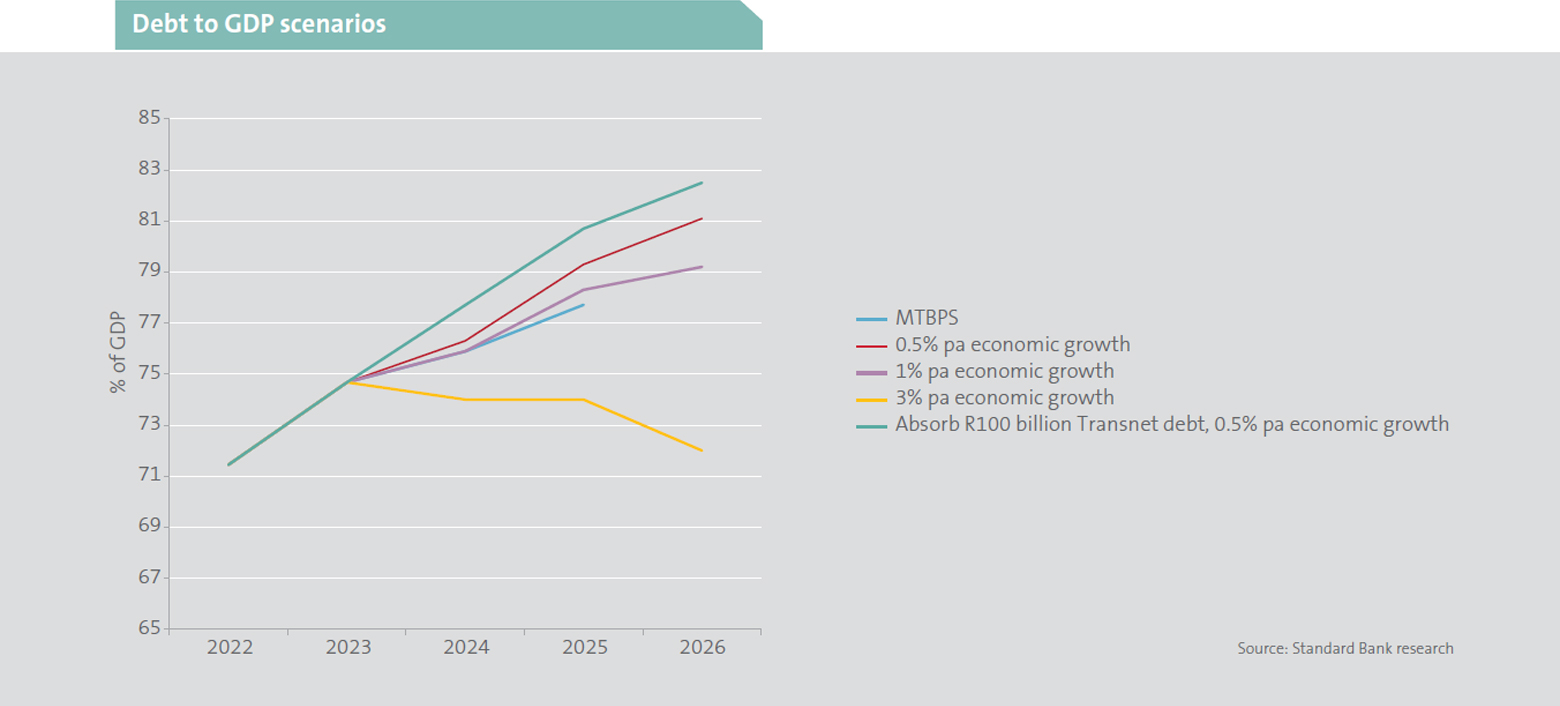

It is beyond the scope of this article to propose solutions to foster faster growth, but reforming the economy’s constraints and inefficiencies most likely reside in many domains and primarily involve freeing up the private sector and improving government service delivery. The chart below shows potential outcomes based on different growth and spending scenarios and the quantum of higher growth levels’ impact on improving the debt/GDP metric.

A comparison of spreads to other countries

Assessing sovereign credit risk across similar countries can be done by comparing credit ratings to CDS spreads. South Africa’s CDS spreads currently trade at levels slightly higher than similar rated countries. However, as important as the current country rating is, it is the trajectory of that rating that is more significant in the analysis. South Africa’s stable outlook compares to the stable outlook of Brazil, Columbia, Thailand and Mexico, all of which have lower CDS spreads and higher credit ratings. Additionally, countries like Brazil have a higher debt/GDP ratio than South Africa, yet sovereign risk spreads are much lower, indicating that a better path to fiscal improvement is being envisaged by markets and priced into its CDS spread.

If economic growth can accelerate, South Africa could see its rating outlook improve and forward-looking market CDS spreads move lower.

The key weakness relating to South Africa’s sovereign credit risk is its fiscal position. The potential outcomes for fiscal consolidation have many constraints but a higher economic growth trajectory over the medium term is critical. We view the sovereign credit risk premium component to be fairly priced, given the weak fiscal position and risks to the outlook, yet an improving situation is possible. We therefore see substantially more value in buying rand-denominated government bonds. These are pricing in a very high currency risk premium, therefore offering rich real yields. The US Treasury yield curve should also move lower as inflation is brought under control in the US, boosting returns.