Dirk van Vlaanderen – Portfolio Manager

The recipe for beer has remained unchanged for thousands of years. Water, barley, hops and yeast continue to be combined in breweries all over the world to create this popular, refreshing beverage. However, industry trends suggest that consumers young and old are drinking less beer, demanding a greater variety of beverage products and migrating to other beverage categories (ie spirits or wine). This is placing downward pressure on beer volumes, particularly in mature markets.

Focusing on the world’s largest brewer, Anheuser-Busch InBev (ABI), we explore how the world of beer is evolving, how this could test the traditional industry fundamentals and how brewers are adapting to these trends.

Beer growth outlook is fizzling out

The size of the global beer market is often analysed as the number of people of legal drinking age and the per capita consumption (PCC) of these drinkers. The PCC of a market is typically influenced by the income level of its consumers and their age. Consumption tends to rise as income levels increase and younger consumers (18 to 35 years of age) tend to drink more.

As indicated below left, global beer volumes have averaged around 2% growth per annum for the past 140 years, with only one 10-year period (coinciding with the First World War) showing negative growth. Colonial expansion in the late 1800s brought beer to all corners of the globe and the rapid economic and population boom in Europe and North America from 1950 to 1970 helped reignite volumes worldwide. The baton then passed to Eastern Europe and China as primary regions of growth in the late 1990s and early 2000s.

Large market contributors to global beer volume growth over the past 50 years have now matured. PCC levels have been dropping from their peak in 2007 (below right). Since the 1980s, the declining trend in North America and Western Europe was largely offset by significant PCC increases in emerging markets (particularly South America, Eastern Europe and China), but now these regions have also mostly matured and, in the case of Eastern Europe, have seen strong PCC declines.

Africa and South-East Asia are the last bastions of strong volume growth resulting from young and growing populations and a rising PCC. This will help deliver some volume growth, but at rates well below those enjoyed since Charles Glass first opened the Castle Brewery in Johannesburg in the 1880s.

Despite beer volumes in mature markets either declining or having plateaued, there are pockets of growth in the overall market. Key trends offering opportunity and risk to incumbent brewers include some of the following:

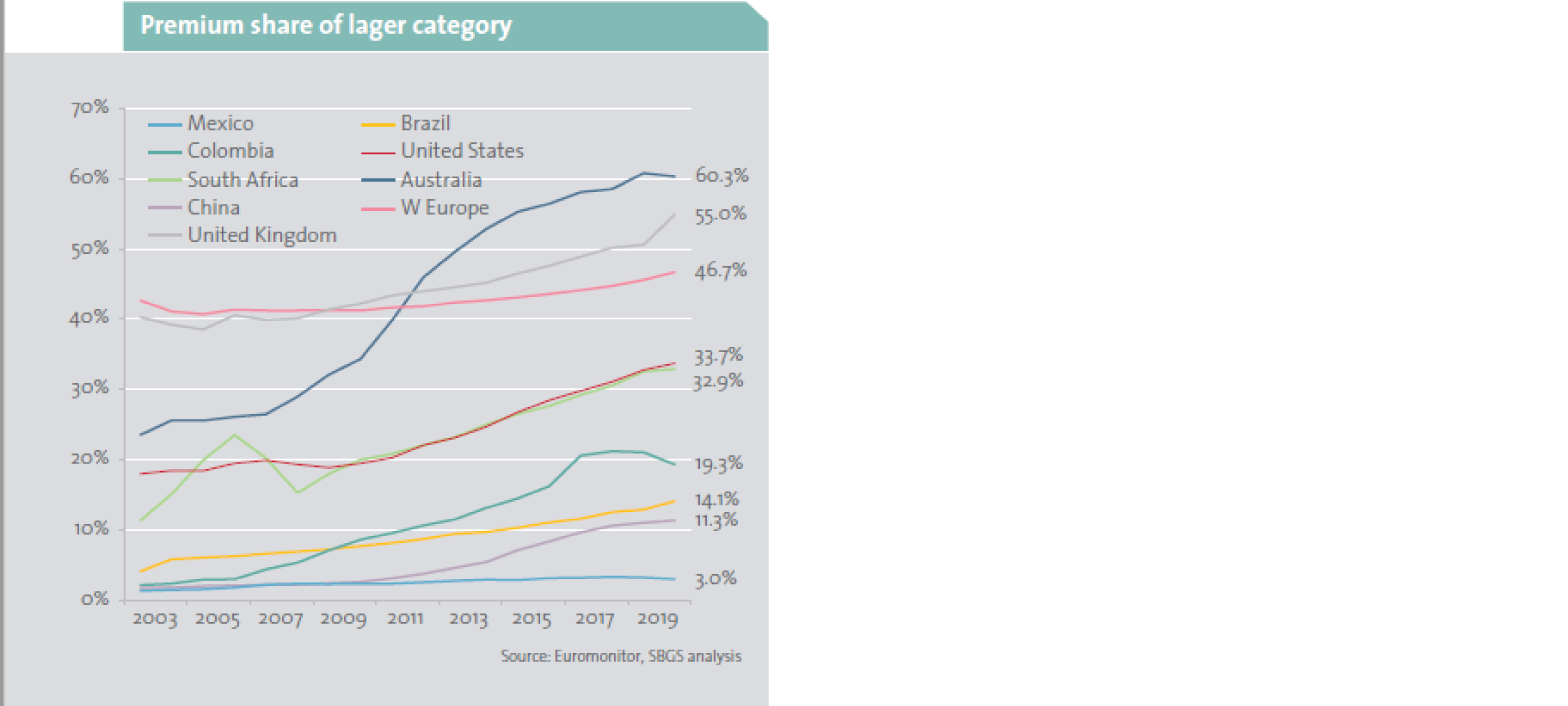

Premium beer: The beer market can be stratified into differing product price points, with economy as the cheapest, followed by mainstream and then premium or super-premium beers. Typically, the cost of producing beer across the price points is not materially different and therefore selling beer at a higher price is more lucrative for the profit margins of the brewers (premium beer is 50%-70% more profitable per liter than mainstream). Unsurprisingly, as volumes have slowed or declined, brewers have sought to trade the consumer up into a more premium beer bracket to improve profits.

As charted below, this strategy has worked well in mature markets like the USA and Europe, where premium beer consumption is now above 30% of the market. It has also been increasingly employed in maturing emerging markets (Latin America, China and Eastern Europe). While beer is traditionally a local-brand business, brewers have been using their global brands to attract higher price premiums – Heineken, Budweiser and Corona are examples of this in practice.

The generational shift away from beer: As people get older, they tend to consume less alcohol and change their preferences towards wine and spirits, resulting in a declining beer PCC. Interestingly, young people are choosing to drink less beer in more mature markets, opting for spirts or other types of popular alcoholic beverages instead. This is demonstrated by the USA, a very mature market where beer’s share of alcohol has reduced from 63% to 47% in just 10 years. This has mainly been to the benefit of spirits, although there has also been a rapid increase in ready-to-drink beverages over the last two years.

The move to near beer: For many years now, brewers have creatively opted to launch “near beer’ offerings, such as radlers1 in Europe or flavoured beers like Flying Fish in South Africa. More recently, low- or non-alcoholic beer has gained market share, with Heineken Zero leading the charge. Low alcohol beers are extremely profitable as they don’t attract any excise tax but are priced the same as alcoholic beers.

The last three years have largely been characterised by the rise of hard seltzers2 in the ready-to-drink category, most pronounced in the USA with the initial success of the White Claw brand (owned by Mark Anthony Brands) and competitors following suit. Hard seltzers have stolen more than a 10% share from the beer market in under four years, which is a considerable feat. While of the same alcohol content as beer, hard seltzers are significantly lower in calories and have, therefore, resonated with the younger, more health-conscious consumers. Near beer innovations are also increasingly targeted at the female segment of the market, which has traditionally not been well enough addressed by the brewing industry. These types of beverage innovations are allowing brewers to sell more profitable products to offset volume declines in their core, less-profitable mainstream brands.

1This is similar to a shandy.

2Fruit-flavoured sparkling water beverage with an alcohol content similar to that of beer.

All hail the king

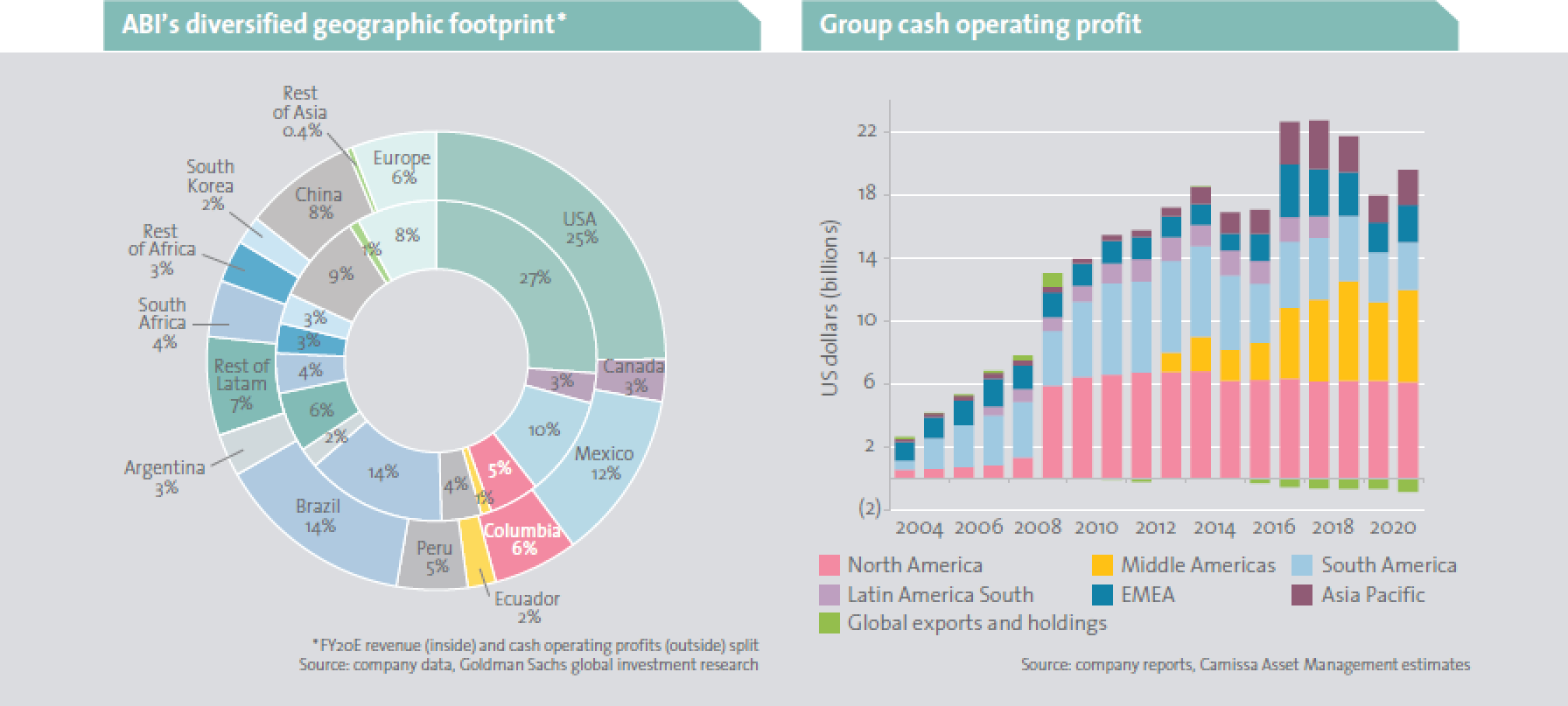

ABI is the world’s largest brewer, formed through several sizable acquisitions – most recently acquiring SABMiller for $107 billion in 2016 – creating a truly global brewing behemoth. Large brands manufactured by ABI include Budweiser, Stella Artois, Corona, Becks and Hoegaarden, however the bulk of their volumes and profits are generated through the significant market shares enjoyed from the portfolio of local brands.

Contributing 25% of operating profit, the USA is ABI’s largest region. Mexico presents a significant market at 12% of profit, followed by a portfolio of Central and South American markets that make up a combined profit of 37% (the largest being Brazil at 14%). The brewer also has a profitable and growing Chinese business and a good footprint in Africa, which although small in profit contribution, is an area for future growth (left chart below).

One deal too many?

Buoyed by the success of integrating previous acquisitions and the significant cost savings generated from applying ABI’s ‘Zero Based Budgeting’ approach, the SABMiller deal was earmarked to incorporate several high-growth markets (ie Africa and Latin America) and provide access to SABMiller’s legendary brand building DNA. The reality has, however, proved very different to expectations.

The $107 billion price tag was mostly funded through hard currency debt and, consequently, the significant post-deal currency devaluation in several of ABI’s emerging markets (particularly Africa and South America) has constrained the company’s ability to reduce this debt. The forced sale of the Australian business, the sale of 50% of the US packaging business and the partial listing of the Asian business has brought in $19 billion in cash. However, $76 billion of net debt3 remains (four times their cash operating profit). In summary, the absolute level of the 2021 cash operating profit for the group is likely to be only marginally ahead of the 2014 level – despite the contribution of profits from the acquired SABMiller business – with an additional debt pileup (right chart below).

Currency woes have been exacerbated by poor in-country performances, once the effect of the SABMiller deal cost cutting measures wore off. This was particularly evident in several African markets and South Africa, where margins have collapsed from post deal highs and market share has been lost at a frightening rate – mostly to Heineken. Heineken’s imminent purchase of Distell will likely result in further market share pain for ABI locally and in surrounding markets.

3Gross financial debt less cash and cash equivalents.

Adapt or die

The cash generation and cost control abilities of ABI is indisputable, but the company needs to shift strategy to focus more on sustainable revenue, which requires patience and time. While the business has been adapting to the trends discussed, this adds a level of complexity (and cost) that essentially detracts from the traditional high volume/low-cost operating model for beer. The near beer opportunity also comes with the risk of new entrants as seen in the USA (with White Claw) and breaks down beers’ traditionally large competitive moats.

The world of beer as we have known it for centuries is clearly changing. Consumers are demanding greater choice, the lines of beer versus other beverages are blurring and key growth engines are slowing. While ABI is adapting to developments and increasing their focus on revenue, the jury is still out as to whether the much-lauded brand-building culture of SABMiller remains within the group, along with the patience needed to allow this to shine through. Currently, our clients do not have exposure to ABI.